If you’re planning to take a home loan in India in 2025, finding a lower interest rate can save you lakhs over the tenure of the loan.

But with so many banks and HFCs competing, how do you pick the lender with the best rate, legal terms, and actual value?

Scroll down—we’ve researched the latest official data (July 2025) and broken it down into a helpful, legal-level guide.

📉 Why Choosing the Right Interest Rate Is Crucial

- A lower rate significantly reduces your EMI burden and total interest paid.

- It helps in reducing housing loan affordability stress.

- In case of floating rates, lower base rates shield you from sharp EMI hikes.

Under Indian law, lenders must disclose official interest tables, processing fees, and any change in rate linked to benchmarks like RLLR or MCLR.

🏦 Which Banks Offer the Lowest Rates in July 2025?

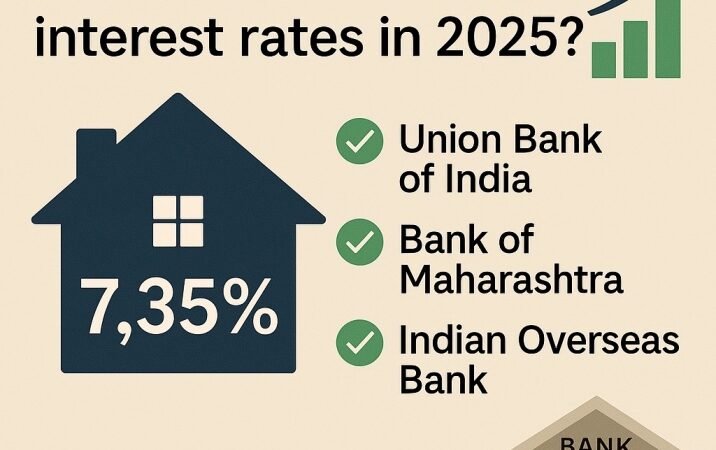

Union Bank of India

Bank of Maharashtra

, and

Indian Overseas Bank

Offer the lowest home loan starting rates at ₹7.35% per annum .

Bank of India

Bank of Baroda

Punjab National Bank

Canara Bank

Have rates starting from ₹7.40%–7.45% .

Major public sector banks like SBI and LIC Housing Finance

Offer rates around 7.50% onwards and typically come with transparent legal structures and benchmark-linked resets .

Private banks such as HDFC and ICICI

Offer rates from ~8.15% to 8.75%, depending on credit profile and digital processing .

⚖️ Key Legal & Professional Considerations Beyond Rate

🔄 Interest Rate Linked to Benchmarks

- Banks may offer loans tied to Repo-Linked Lending Rate (RLLR) or MCLR; you must check which applies.

- Changes in RBI’s repo rate will impact floating rate loans. For instance, SBI recently cut its MCLR by 25 bps, potentially lowering EMI for borrowers .

📋 Processing and Hidden Charges

- Even if the interest is low, processing fees, prepayment charges, and foreclosure penalties can add substantially.

- Public banks often have zero or low processing fees (~0.25–0.5 %), while private banks may charge up to 2% plus GST .

✅ CIBIL Score and Borrower Profile

- Top rates (~7.35%) are typically reserved for borrowers with excellent credit (700+), low FOIR, and verified income.

- A slightly higher rate may apply if your credit score or stability is lower .

🛡️ Loan Terms That Affect Your Bottom Line

- Check cases where banks pre-approve loans with no prepayment penalty or offer balance transfers.

- Some lenders provide special schemes for women, government employees, or PMAY beneficiaries, which may waive processing or offer rate discounts .

🧭 Quick Comparison Table

| Bank / Institution | Starting Rate (p.a.) | Processing Fees | Benchmark Type |

| Union Bank of India | 7.35% | ~0.50% + GST (max), or Nil | MCLR |

| Bank of Maharashtra | 7.35% | Nil–0.50% | MCLR |

| Indian Overseas Bank | 7.35% | ~0.50% | MCLR |

| Bank of India / PNB / Canara | 7.40%–7.50% | ~0.35%–0.50% | MCLR |

| SBI / LIC Housing Finance | 7.50% onwards | ~0.35% | RLLR |

| HDFC / ICICI / Private Banks | 8.15%–8.75% | Up to 2% + GST | Bank’s own benchmark |

🧠 How to Legally & Safely Secure the Lowest Rate

1.

Check Benchmark Rate Transparency

- Verify whether the rate is variable or fixed.

- Request a clause in the loan agreement specifying how rate resets happen.

2.

Validate Credit Score & Documentation

- Banks often verify your income, PAN, Aadhaar, bank statements, and property title before finalizing any rate.

3.

Negotiate Terms

- Sometimes banks allow rate negotiation; a small reduction in spread or waiver of processing fee can offer substantial savings.

4.

Watch for Rate Cuts

- Monitor RBI repo rate announcements. Lenders typically pass benefits with a delay — keep an eye on reset dates.

📝 Final Word

As of July 2025, Union Bank of India, Bank of Maharashtra, and Indian Overseas Bank lead with home loan rates as low as 7.35% p.a. .

But remember: a lower rate alone doesn’t guarantee the best outcome.

Always read the fine print, confirm legal terms around rate resets, processing charges, and foreclosure clauses.

📩 Call to Action

Need help picking the right bank or evaluating a home loan offer?

At RJ Property Law, we provide:

- Legal review of loan agreements

- Comparison of lender terms and hidden clauses

- Advice on interest reset links and documentation

- Assistance for NRI or PMAY-linked loans

📧 Email: ranjinijayaram@rjpropertylaw.com

📞 Call: +91 80884 17193

🌐 Visit: www.rjpropertylaw.com

✅ Borrow smart. Borrow legally. Borrow with clarity.